Rewards and penalties

Liquidity providers earn rewards for providing enough liquidity.

If you are an LP and you can’t support your liquidity commitment financially, you will be penalised.

If you don't have liquidity on the book to meet the minimums required by the SLA, you won’t receive any rewards and will also be penalised.

Rewarding liquidity providers

Liquidity providers earn from the fees paid by takers on the market. How much you are rewarded depends on:

- Your relative commitment

- How early in the market’s lifecycle you committed

- How you perform against the liquidity SLA

Note: During an auction uncrossing, an LP’s orders will not need to provide liquidity or enable trades. However, you must maintain your liquidity commitment, and orders are placed back on the order book when normal trading resumes.

Community-funded LP rewards

In addition to the income made from fees, anyone can fund reward pools that will pay out to liquidity providers at the end of each epoch, based on the proportion of fees the LPs have received.

Concept: Rewards: Learn more about community funded LP rewards, and trading rewards in general.

Earning liquidity fees

Liquidity providers receive a cut of the fees paid by price takers on each trade.

The amount each liquidity provider receives depends on:

- The percentage of a trade's value that is collected from the price taker for each trade, and combined in a pool to be paid to liquidity providers. This is called the liquidity fee

- Performance against the liquidity SLA, which defines what percentage of your bond is used to provide orders, and for how long it needs to be on the book. If you do not meet the SLA minimum, you do not get any revenue from the liquidity fee

- Your equity-like share of the market, which is based on the relative size of their commitment amount, and when you committed liquidity to the market. Liquidity providers who commit to a market early benefit from helping to grow the market by getting a higher share of the fee revenue

- LP’s liquidity score, which is the average volume-weighted probability of trading of all their orders within the liquidity order price range

Read more about how it works: Dividing liquidity fees among LPs

Liquidity SLA

When committing to provide liquidity, you enter into an agreement to receive a portion of fees paid by traders in return for keeping the market liquid.

The terms of that agreement, called the liquidity SLA, are that each LP needs to have a certain percentage of their commitment amount on the order book for a minimum amount of time in each epoch.

Doing less than the minimum means liquidity fee payments will be withheld for that epoch, it will have an impact on future fee revenue earnings, and a sliding penalty will be applied to your bond. Everything at, or above, the minimum means some amount of your accrued fee amount will be paid. The better you do against the SLA, the more fee revenue you'll receive.

The percentage of your commitment amount and minimum time are set for each individual market. You can query a market details or review a market's governance proposal to see the SLA requirements.

These include:

LP price range: The allowed spread either side of the mid price for LP orders For example, if this is set to 0.01, LPs must place orders within 1% of the mid price for them to count towards their liquidity commitment time on the book.

Minimum time fraction: The percentage of the time during each epoch that an LP must have at least their committed volume of orders on the book. Below this they will be penalised, at a minimum by loss of all accrued fees for the epoch.

Hysteresis epochs: The number of epochs for which an LP will continue to receive a penalty after failing to meet the SLA. At the end of any given epoch the penalty is defined as the maximum of either the penalty for the just completed epoch or the average penalty across other epochs in the hysteresis window.

Competition factor: Controls the extent to which an LP outperforming other LPs in time spent on the book will receive a larger share of rewards.

And these network parameters, which also impact LP rewards, are set system wide:

- market.liquidity.sla.nonPerformanceBondPenaltyMax: Specifies the maximum fraction of an LP’s bond that may be slashed per epoch for failing to meet their SLA commitment. When this is set to zero, liquidity bonds are not at risk of slashing.

- market.liquidity.sla.nonPerformanceBondPenaltySlope: Specifies how aggressively the penalty is applied for underperformance (for example: a slope of 1.00 means that for every 1% underperformance 1% of the bond is slashed, up to the maximum above, whereas a slope of 0.1 would mean that for every 10% underperformance the bond would be slashed by 1%).

- market.liquidity.earlyExitPenalty: This defines the amount of an LPs bond that will be kept if they cancel their commitment while the market is below its target stake of committed liquidity. If the cancellation is partial or takes a market from above to below target stake, only the pro-rata portion of the bond related to the removal of liquidity below the target stake will be assessed for the penalty.

Determining the liquidity fee percentage

Market proposers can set how the liquidity fee charged to traders is calculated.

There are three options:

- Constant fee

The market's liquidity fee is provided in the market proposal and this percentage doesn't vary.

- Stake-weighted-average of submitted fees

Each liquidity provider submits their desired liquidity fee factor in the liquidity commitment transaction. It’s a number between 0 and 1. Each fee factor has a weight assigned to it based on the supplied liquidity from each provider. The fee factor that's used is the weighted average of all those submitted. The final fee factor is converted into a percentage.

In the example below, three liquidity providers bid for their chosen fee factor. The final factor is the stake-weighted average of the three.

[LP 1 stake = 120 ETH, LP 1 liquidity-fee-factor = 0.5%][LP 2 stake = 20 ETH, LP 2 liquidity-fee-factor = 0.75%] [LP 3 stake = 60 ETH, LP 3 liquidity-fee-factor = 3.75%]

then

liquidity fee factor = ((120 0.5%) + (20 0.75%) + (60 * 3.75%)) / (120 + 20 + 60) = 1.5%

Marginal cost

a. Each liquidity provider submits their desired liquidity fee factor in the liquidity commitment transaction. It’s a number between 0 and 1. The final fee factor is converted into a percentage. Every LP’s proposed fee factor goes into determining the actual fee each trader will pay on a trade in that market.

b. The liquidity orders submitted are sorted into increasing fee order so that the lowest fee percentage bid is at the top, and the highest is at the bottom.

c. The market's 'winning' fee depends on the liquidity required for the market (target stake) and the amount committed from each bidder. The protocol processes the LP commitments from top to bottom, adding up the commitment amounts until it reaches a level equal to, or greater than, the target stake. When that point is reached, the proposed fee that was provided with the last processed liquidity commitment is used. Initially, before a market opens for trading, the market's initial liquidity fee is the lowest proposed, because the market’s target stake is zero.

d. Once the fee for the market is set, all liquidity orders charge that fee, regardless of whether the provider's submitted fee was higher or lower, and whatever the proposed fee factor.

e. This fee percentage can change. Once the market passes governance and its opening auction begins, a clock starts ticking. The protocol calculates the target stake, and the fee is continuously re-evaluated. Liquidity providers amending or cancelling their commitments will also lead to the fee factor changing.

Liquidity fee example

In the example below, there are 3 liquidity providers all bidding for their chosen fee level, with the lowest fee bid at the top, and the highest at the bottom.

- [LP 1 stake = 120 ETH, LP 1 liquidity-fee-factor = 0.5%]

- [LP 2 stake = 20 ETH, LP 2 liquidity-fee-factor = 0.75%]

- [LP 3 stake = 60 ETH, LP 3 liquidity-fee-factor = 3.75%]

- If the target stake = 119 then the needed liquidity is given by LP 1, thus the market's liquidity-fee-factor is the LP 1 fee: 0.5%.

- If the target stake = 123 then the needed liquidity is given by the combination of LP 1 and LP 2, and so the market's liquidity-fee-factor is LP 2 fee: 0.75%.

- If the target stake = 240 then all the liquidity supplied above does not meet the estimated market liquidity demand, and thus the market's liquidity-fee-factor is set to the highest, LP 3's fee: 3.75%.

Dividing liquidity fees between LPs

Distribution of fees between LPs is performed in several steps, first at the time of a trade and then with a final rebalancing at the end of each epoch.

Probability of trading: For each price level, the risk model implies a probability of trading based on the cumulative distribution of a lognormal function between the tightest price monitoring bounds currently for the market and best bid/ask. The network parameter market.liquidity.minimum.probabilityOfTrading.lpOrders defines a minimum value for the probability of trading at a given price level.

- Parameters

mu,tauandsigmaare taken from the individual market's risk model, additionallytau_scalingis taken from the relevant network parameter market.liquidity.probabilityOfTrading.tau.scaling - For a price on the buy side, calculate the cdf between

min_valid_price(the lowest price within the tightest price monitoring boundaries) and theprice, normalising for a sum of1betweenmin_valid_priceandbest_bid. - For a price on the buy side, calculate the cdf between the

priceandmax_valid_price(the highest price within the tightest price monitoring boundaries), normalising for a sum of1betweenbest_askandmax_valid_price. - Define a lognormal distribution

Dwith:- scale =

sigma`sqrt(tau tau_scaling)` - loc =

exp(log(best_price) + (mu - 0.5 * sigma ^ 2) * tau * tau_scaling)(wherebest_priceisbest_bid/askdepending on whether considering the buy or sell side.)

- scale =

- Calculate the CDF of distribution

Dat thelower_bound(min_valid_pricefor buy side andbest_askfor sell side) and at the upper bound (best_bidfor buy side andmax_valid_pricefor sell side). - Define

z, a scaler, to beCDF(upper_bound) - CDF(lower_bound) - Probability of trading is then:

- For a buy order,

P(t) = 0.5 * (CDF(price) - CDF(lower_bound)) / z - For a sell order,

P(t) = 0.5 * (CDF(upper_bound) - CDF(price)) / z

- For a buy order,

- If probability of trading <

minProbabilityOfTrading, return the valueminProbabilityOfTrading

- Parameters

Initial fee distribution:

- Liquidity score is used for initial fee distribution between LPs at trade time. It is recalculated frequently:

- For each LP, each of their orders within the SLA bound is assessed. For each price level, the probability of trading is calculated as above. For each order included, the LP's volume is multiplied by the probability of trading at that price. These are then summed up to generate a notional liquidity score.

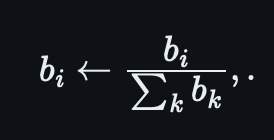

- These are then normalised across all LPs. i.e.

fractional instantaneous liquidity score = instantaneous liquidity score / total scores across all LPs - An LP's iquidity score is then updated to be a weighted sum of the previous liquidity score and the new instantaneous one:

liquidity score <- ((n-1)/n) x liquidity score + (1/n) x fractional instantaneous liquidity score

- Liquidity score is used for initial fee distribution between LPs at trade time. It is recalculated frequently:

For fee distribution, each LP receives a portion equal to

LP Equity-like Share * LP Liquidity Score, normalised across all LPs.Under 100% time-on-book

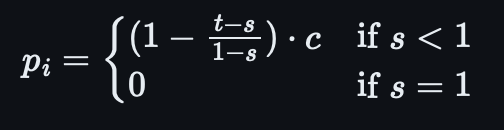

- If an LP meets the SLA criteria but is under 100% time on book, they may have some portion of their fees redistributed. This is calculated with the equation below, where 't' is their fraction of time on the book, 's' is the minimum SLA fraction and 'c' is the competition fraction discussed above. 'p' then gives the fraction of fees redistributed.

- If an LP meets the SLA criteria but is under 100% time on book, they may have some portion of their fees redistributed. This is calculated with the equation below, where 't' is their fraction of time on the book, 's' is the minimum SLA fraction and 'c' is the competition fraction discussed above. 'p' then gives the fraction of fees redistributed.

Fee redistribution

Any fees not immediately paid out to LPs as a result of under 100% time on book are redistributed in a few steps. First each LP receives a weight according to their proportion of fees that epoch.

Then that score is updated by multiplying by their SLA penalty as calculated above.

Then these are finally re-weighted across all LPs.

Each LP then receives this fraction of the garnished SLA funds as a final bonus.

How liquidity fees are distributed

The liquidity fee amount is collected from traders on every trade, and held in a separate account. This account is under the network’s control.

How often fees are distributed is defined by the network parameter market.liquidity.providersFeeCalculationTimeStep. Starting with the end of the market's opening auction, every time the time-step has been hit, the balance in the account is transferred to each liquidity provider's margin account for the market. This depends on your share and how well you performed against the SLA.

Fee distribution example

A market has 4 LPs with equity-like share. Each LP has the same liquidity score and meets but does not exceed the SLA:

- LP 1 share = 0.65

- LP 2 share = 0.25

- LP 3 share = 0.1

Participants trade on the market, and the trade value for fee purposes multiplied by the liquidity fee factor equals 103.5 ETH (the market's settlement asset).

Thus, the following amounts are then transferred to each LP's margin account once the time-step elapses:

- LP 1 receives: 0.65 x 103.5 = 67.275 ETH

- LP 2 receives: 0.25 x 103.5 = 25.875 ETH

- LP 3 receives: 0.10 x 103.5 = 10.350 ETH

Penalties for not fulfilling liquidity commitment

Penalties for not meeting SLA

Not meeting the SLA deprives you of all liquidity fee revenue, and a sliding penalty is applied to your bond amount. How much penalty is based on the value of the network parameter market.liquidity.sla.nonPerformanceBondPenaltySlope. It determines how steeply the bond penalty increases linearly, until it reaches the maximum. The maximum penalty that can be charged is capped by the market.liquidity.sla.nonPerformanceBondPenaltyMax network parameter.

See the full calculation in the setting fees and rewarding LPs spec ↗.

Not meeting the SLA will also affect future fee revenue, even in epochs when the SLA is met. The number of epochs that are used to determine performance is called the performanceHysteresisEpochs. This number is defined in a market's parameters. If the parameter is set to 0, it will only count the just-completed epoch. If set to 1, the fee revenue is impacted by the just-completed epoch and the one before.

If you decrease or cancel your liquidity commitment below the market's target stake, you may forfeit some of your bond. This is called the early exit penalty.

You can query a market details or review a market's governance proposal to see how the past performance will impact rewards, and what the early exit penalty is set at.

Penalties for not supporting orders

Not being able to support the orders you posted using funds in your general and/or margin accounts will put you at risk of closeout, and can put the market into a situation where there is not enough liquidity.

If the liquidity provider's margin account doesn't have enough funds to support the orders, the protocol will take funds from your liquidity commitment bond to cover the shortfall. A penalty will be applied, and funds to cover the shortfall and pay the penalty will be transferred from the provider’s bond to the market's insurance pool.

The liquidity obligation will remain unchanged and the protocol will periodically search the liquidity provider's general account and attempt to top up the bond account to the amount specified in your liquidity commitment.

Should the funds in the bond account drop to 0, you will be marked for closeout and your orders will be cancelled. If this happens while the market is transitioning from auction mode to continuous trading, you will not be penalised.

Calculation of penalty for not supporting orders

The penalty formula defines how much will be removed from the bond account:

bond penalty = market.liquidity.bondPenaltyParameter ⨉ shortfall

- market.liquidity.bondPenaltyParameter can be changed through governance.

- shortfall refers to the absolute value of the funds that:

- the liquidity provider was unable to cover through margin and general accounts

- are needed for settlement

- are needed to meet the margin requirements